February 2026 was one of the most turbulent months on record for bitcoin mining metrics, marked by an all-time low in dollar-denominated hashprice, a historic whipsaw in mining difficulty, and the steepest BTC price decline since 2021.

The combination of these forces created an operating environment unlike anything miners have seen outside of the summer of 2021 in the aftermath of China’s bitcoin mining ban. Analysts at Luxor break down all of the key details from the month in their latest Hashrate Lookback Series.

You’re reading a recap of Luxor’s February Hashrate Lookback Series. You can download the full report via the form below:

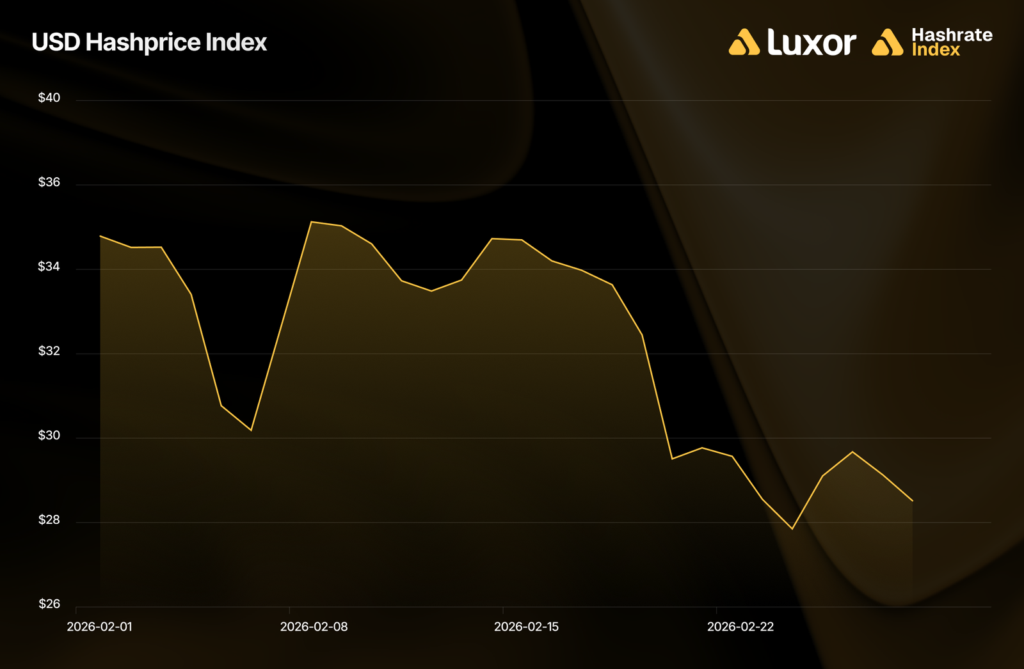

Hashprice hits an all-time low

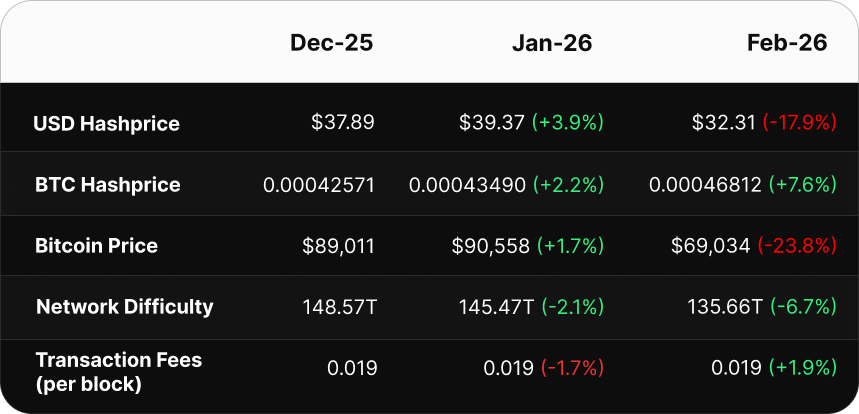

Per Luxor’s report, the month’s most significant development was hashprice reaching an all-time low of $27.89/PH/day on February 24.

Bitcoin’s steep drop in price was the primary driver compressing hashprice in February. Bitcoin opened the month at $78,073 and spent the next four weeks sliding to a close of $65,204, representing a 23.8% monthly decline and a monthly average of roughly $69,000. The nadir of this selloff was $63,000, marking a 50% drawdown from bitcoin’s October 2025 all-time high.

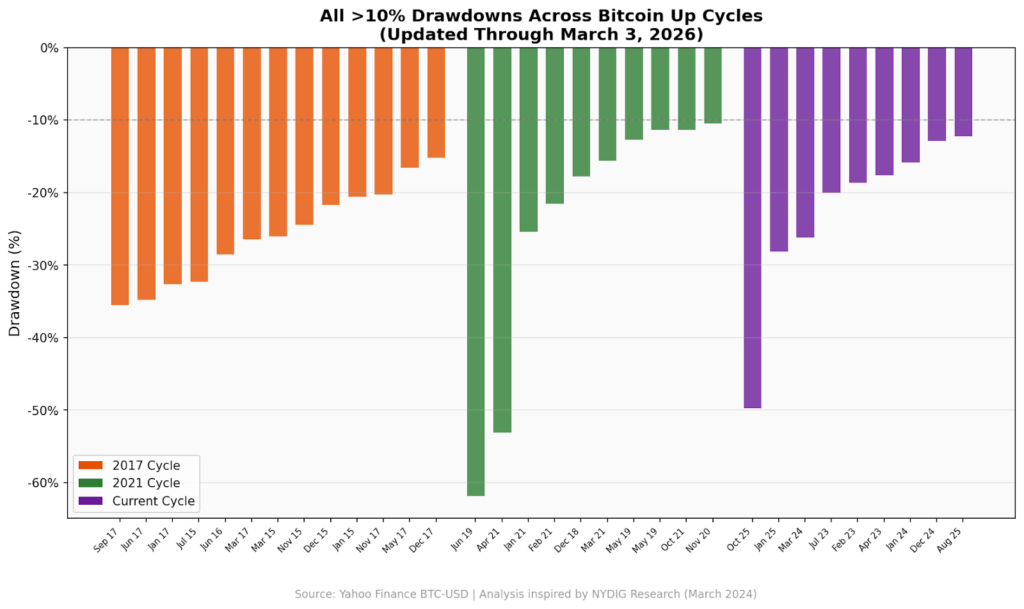

The February decline was the continuation of a broader sell-off that has now become the deepest correction of the current cycle. On the way down, bitcoin experienced its 9th 10%+ drawdown since the cycle’s trough of $15,460 in November 2022.

While painful, the research notes that corrections of this magnitude are a recurring feature of bitcoin bull cycles, not an anomaly.

Bitcoin’s fall takes mining difficulty for a ride

All of that price volatility created historic turbulence for bitcoin’s mining difficulty, what the reports calls the “whipsaw” effect.

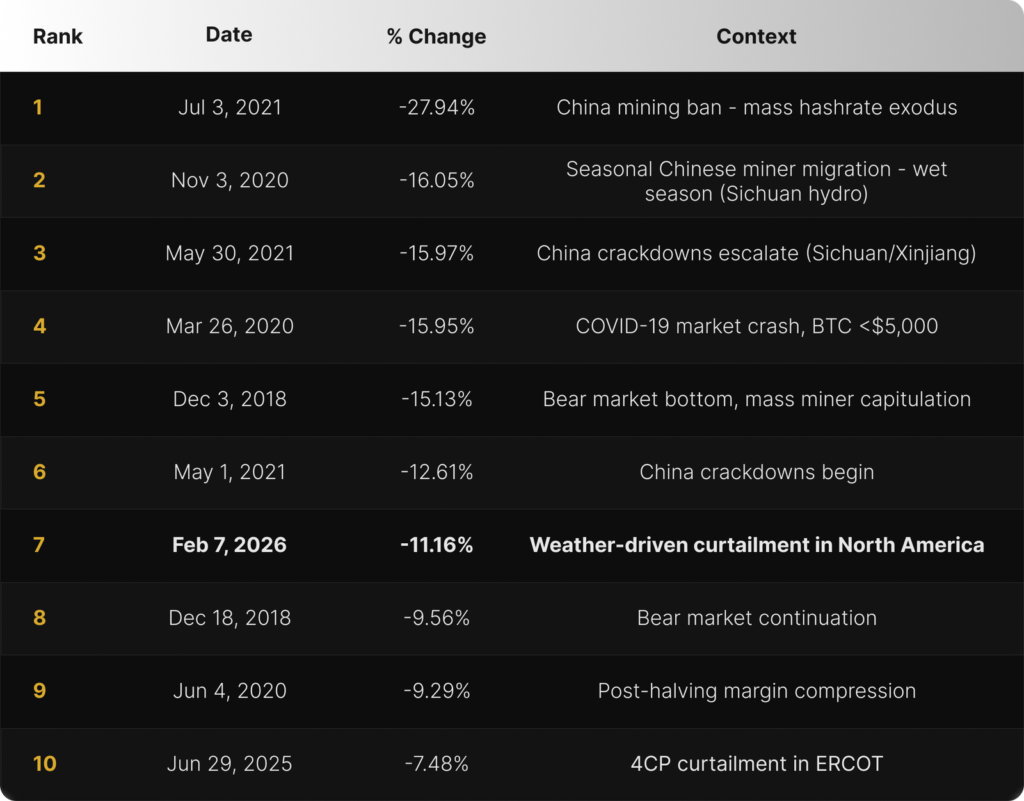

The month began with miners being frosted over by Winter Storm Fern, the most severe Winter Storm since Jonas in 2016. Following weather-driven curtailment events across North American power grids in late January, a significant portion of the network’s hashrate went offline as power prices in ERCOT and neighboring grids temporarily exceeded mining profitability thresholds.

The resulting shortage of active hashrate produced a downward difficulty adjustment of 11.16% on February 7th — the seventh-largest negative adjustment in the modern ASIC era (defined in the report as 2016 onward) and the largest single-epoch drop since the July 2021 China ban.

Just twelve days later, as temperatures normalized and curtailed machines came back online, the network swung back hard with a 14.73% upward adjustment on February 19th, the twelfth-largest positive move on record in the post-2016 period.

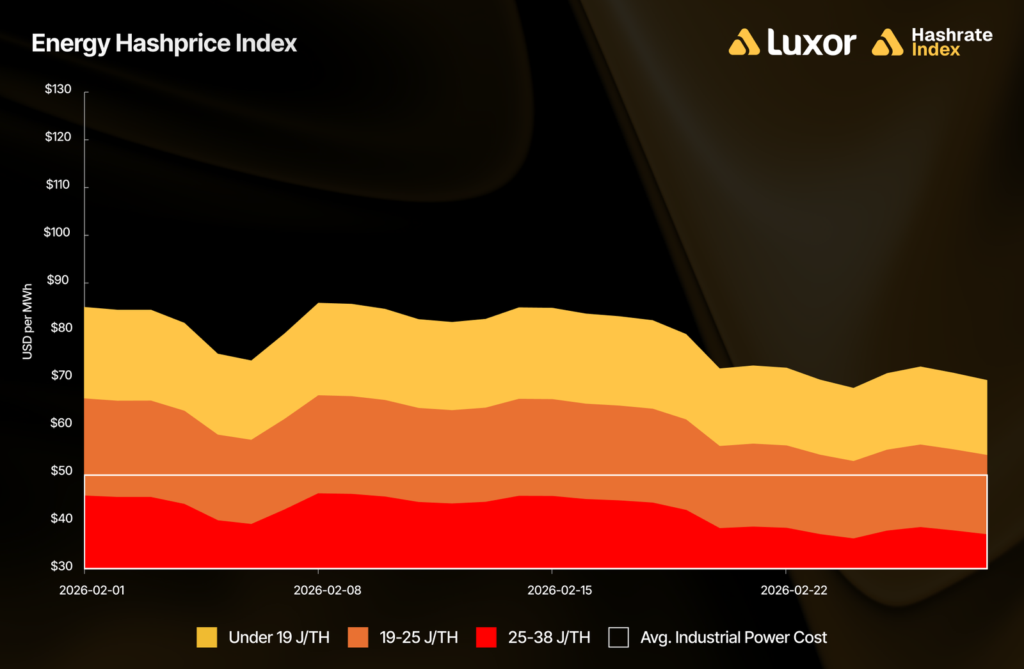

With hashprice squeezed from both ends by bearish price action and a rising difficulty, older generation ASIC hardware is treading water. Implied mining revenue per unit of electricity consumed was approximately $79 per MWh for the most efficient fleets (those with energy efficiency under 19 J/TH), dropping to $61 per MWh for mid-tier operations (19–25 J/TH) and $42 per MWh for older machines in the 25–38 J/TH range.

With an estimated network-average power cost of $50 per MWh, any fleet operating at or above the S19-era efficiency threshold ran at a gross loss for the entire month. BTC hashprice, which moves inversely to difficulty, offered a modest counterpoint: the monthly average rose 7.6% to 0.00047 BTC per PH/s/day, providing some nominal relief to miners who track their economics in BTC terms rather than dollars.

The Hashrate Index report concludes by estimating that, under current bitcoin mining economics, there is little room for hashrate growth in 2026.