Wall Street has found its favorite Bitcoin trade, and it isn’t buying Bitcoin.

The BTC treasury boom is turning bust, with the most popular bitcoin treasury companies are down 50% over the last six months, but one group in particular has profited despite the drooping sentiment.

A few months removed from the euphoria of the bitcoin treasury peak, it’s becoming clear that the banks were one of the few winners in the whole saga. Case in point: bankers have likely minted anywhere from $280-560 million from Strategy’s (NASDAQ: MSTR) fundraising events – and that’s just in 2024 and 2025.

Investment banks TD Securities, Barclays Capital, and many more have quietly hauled in hundreds of millions in fees running Strategy’s (NASDAQ: MSTR) firehose of common equity, preferred shares, and convertible notes, while newcomer bitcoin treasury vehicles like KindlyMD / Nakamoto Holdings (NASDAQ: NAKA) show how 2025’s Cambrian explosion of bitcoin treasury companies – which were such a bludgeon to investors – were a boon to investment banks.

How banks win big on bitcoin treasury fundraising

A quick primer on the bitcoin treasury flywheel from the pioneer itself, Strategy

Since 2021, Strategy has used issued at-the-market (ATM) offerings, a fundraising vehicle that allows the company to perpetually sell its stock on the open market, for tens of billions of dollars. According to SEC filings, between January 1, 2024 and September 31, 2025 alone, Strategy sold $28.23 billion worth of stock in ATMs, mostly from its common stock MSTR, but in 2025, also from its new dividend-paying preferred shares STRK, STRF, STRC, and STRD.

In addition to ATMs, Strategy also frequently taps convertible note offerings to raise capital. When a company issues a convertible note, it gives the lender the option to redeem the debt upon maturity in shares of the company’s stock, typically in exchange for a low interest rate.

Strategy plumbs all of these fundraising options to purchase bitcoin in an effort to drive up MSTR’s price so that they can raise more capital. But behind the scenes with each new capital raise, whether an ATM or convertible note, a small circle of investment banks books recurring revenue.

Per SEC filings, Barclay’s, TD, and other banks clip “up to [2%]” on every dollar of Strategy stock they sell. (Neither Strategy nor these banks disclose the exact fee in public filings).

If we take a 1-2% fee range, investment banks could have conceivably earned $280-$560 million from Strategy’s ATMs in 2024 and so far in 2025.

And overall, it’s been a good deal all around for all Strategy participants, banks and shareholders. Strategy is up 838% over the past five years and 300% over the last two, albeit it’s down -35% YTD and -50% YoY.

For 2025’s freshman class of bitcoin treasury companies, though, Strategy’s strategy hasn’t netted the same success so far, but the banks are doing alright.

2025’s class of bitcoin treasury companies tells a different story

Across the broader bitcoin treasury landscape, investors have been steamrolled while the intermediaries (bankers, advisors, and placement agents) are doing fine.

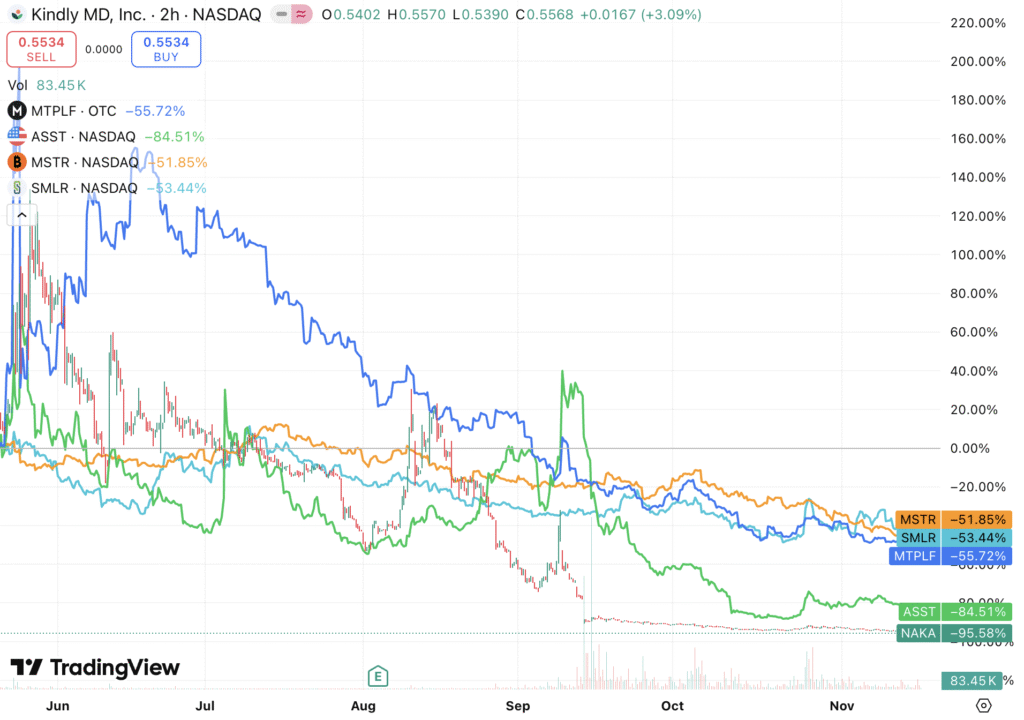

Take the KindlyMD (NAKA) deal. Cohen & Company Capital Markets led the advisory and placement work on the $740 million raise and received $20 million in cash and 11.6 million in NAKA shares.

Hold your pitchforks for a second. The deal was for $20 million in cash and, as reported by Cohen & Company on its Q3 earnings call, $159 million worth of shares at the time the PIPE deal closed and KindlyMD and Nakamoto’s merger closed on August 14, 2025.

On this date, NAKA closed at $13.60, so Cohen’s shares were worth $159 million then. But that stake is worth less than $6.4 million now, and Cohen and Company wrote off the holdings as a $146 million principal transaction loss in its Q3 earnings. KindlyMD CEO David Bailey tweeted that the shares were worth $1.12 when Cohen & Company agreed to the deal. It’s unclear whether or not Cohen & Company has liquidated their shares as of the end of Q3.

While public investors may be up in arms, this is really just the investment bank playbook, and Cohen & Company struck a deal that any other investment bank would have taken in the same situation. Put another way, it’s not their fault NAKA is down 50% since its PIPE offering.

The same pattern repeats across bitcoin treasury offerings. Enormous fundraises pump up headline raise numbers while Wall Street gets commissions off the top. Conventional ATM frameworks put the average cut at 1% – 3% of the raise, and a few public bitcoin treasury deal filings support this convention. (I strongly recommend the BitMex research piece which dives deeper into this)

It’s nuanced though. For deals like NAKA’s PIPE, the lion’s share of banker comp likely has come in stock and is down bad. But banks have also realized hundred of billions in cash portions from bitcoin treasury fundraising commissions.

The bitcoin treasury strategy sector that was inspired by Strategy’s capital machine has all but slowed to a halt, but each ATM, preferred, or convert has added another tollbooth to the road between Bitcoin and Wall Street — now it’s time to see if they’ve become too expensive to use.

Photo by William Warby via Unsplash