Is the bottom in for Nakamoto Holdings (NAKA)? B. Riley Securities analysts think you should buy the dip.

The investment bank has initiated coverage of a handful of crypto treasury companies, per an October 10, 2025 investor memo, and its rating NAKA alongside Sharplink Gaming, BitMine, and other crypto treasury companies as buys.

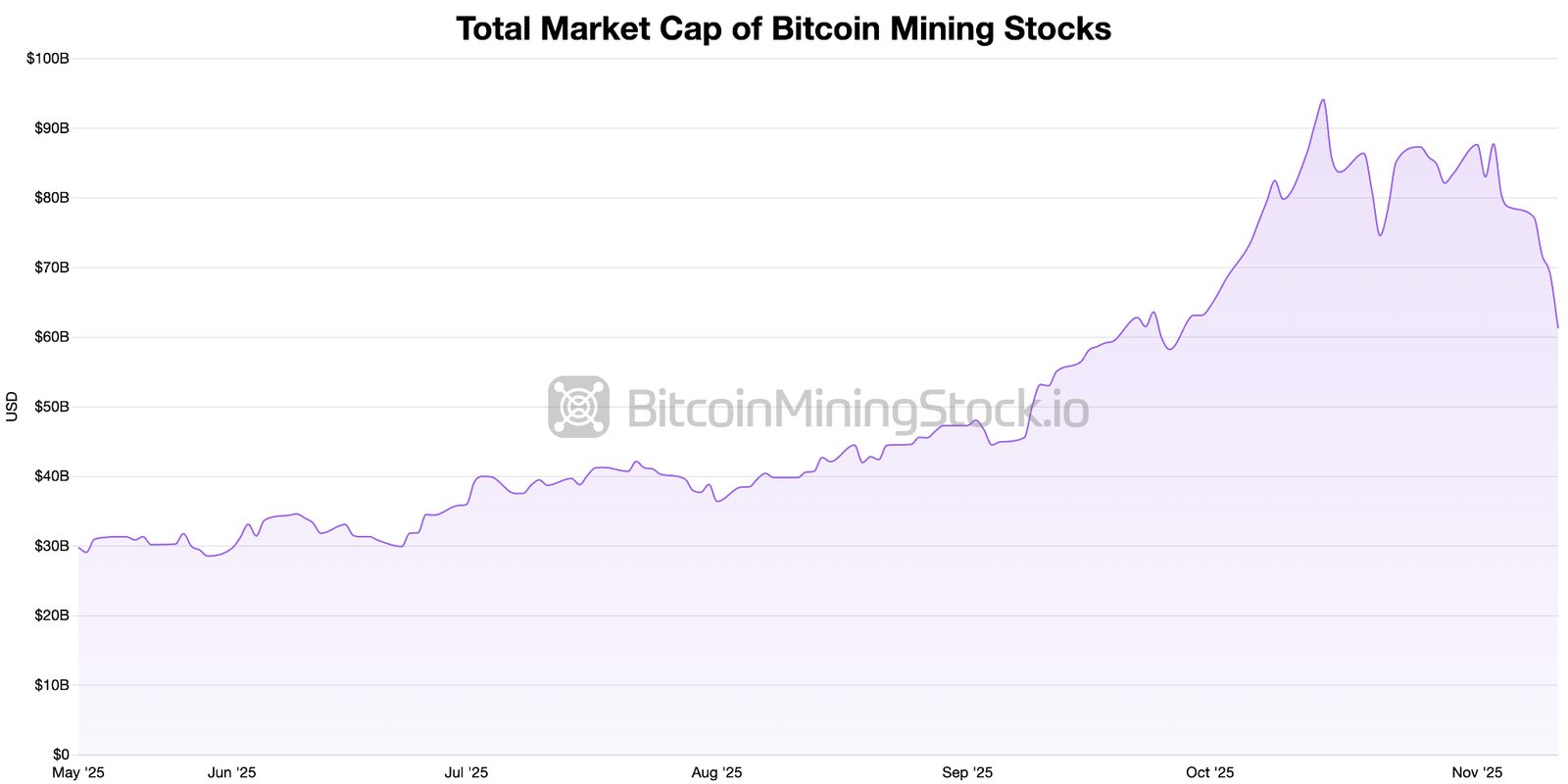

Digital Asset Treasury (DAT) Companies had been second only to AI growth stocks in 2025 for their eye popping returns.

That was until about the year’s halfway point, and it’s been down only for (most) all of these stocks since.

NAKA has been the posterchild of this selloff: the stock is -94% since July 1 and -44% YTD. As B. Riley notes, “the selloff was primarily driven by the announcement of a $5B ATM equity offering, the $30M investment in BTC treasury firm Metaplanet, and heavy insider selling following the expiration of PIPE transaction lock-up periods.”

Following the stock’s bloodletting, the company’s multiple on net asset value – i.e., the total value of the company relative to its bitcoin holdings – was 0.7x as of October 10, 2025, according to B. Riley.

This is below the 1.0x average for NAKA’s peers, the bank notes (Strategy, the creme-de-la-creme of Bitcoin treasury plays, has an mNav of 1.4x currently).

NAKA’s mNAV should correct to the mean, B. Riley argues, “as market perception improves and as accretive BTC purchases boost NAV.” Beyond its Bitcoin stack, B. Riley continues, NAKA could have an edge on upside volatility given its partnership with BTC Inc., the parent company of Bitcoin Magazine and the Bitcoin Conference, which also shares NAKA CEO David Bailey.

Echoing comments that NAKA COO Tyler Evans made to Blockspace in January, BTC Inc. has a vision for “seeding BTC treasury companies in every capital market worldwide.” Should NAKA acquire BTC Inc. as leadership has intimated, this vision, coupled with NAKA’s $30 million stake in Metaplanet and potentially other Bitcoin treasury companies, could boost NAKA’s share price when bitcoin runs.

So the thesis goes, and B. Riley estimates that, “conservatively,” NAKA could appreciate to $2 by the end of 2026, assuming NAKA accumulates ~1,400 BTC using $763 million of a $5 billion open at-the market offering and another 600 BTC before the end of the year.

This would bring NAKA’s total bitcoin holdings to ~18,000 by the end of 2026, worth ~2 billion assuming a bitcoin price of $121,600. At $2 per share, this trove would give NAKA a 1.2x mNAV.

It’s worth noting, as we italicized at the top, the B. Riley has been on the sell-side for NAKA’s at-the market offering, so they are no unbiased party. You could pretty easily drum up a bull and bear case for the stock on market psychology alone:

- Bull: Bitcoin’s price appreciates through 2026 as the dollar debases; now that the PIPE selling is behind it, NAKA can accrue bitcoin with the dry powder it has, and all else being equal, the mNav should recover to 1.0x if bitcoin is doing well – not to mention that the stock has been getting hammered and is likely oversold.

- Bear: Spoiled goods. The PIPE unlock winddown is so brutal as to make some s***coin founders blush. With such a poorly executed and poorly timed first stable at playing the capital markets to accumulate bitcoin, investors might be too skittish to trust the NAKA team to deploy capital efficiently when there are other, more proven options on the table like Strategy and Metaplanet.

At any rate, B. Riley is bullish on a number of crypto treasury stocks, so we may excuse its bias for its confidence in NAKA when we consider that it is bullish on the whole sector. Of all the five DATs it now covers, it issued a buy rating for all of them in its first report and provided mNAV and treasury balance forecasts for these as with NAKA.

For any DAT bagholders needing some hopium, take the huff below chart with a grain of salt — especially considering B. Riley was involved in the raises for Sharplink Gaming and Seuquan in addition to NAKA.