JonesResearch has initiated coverage of Cipher Mining (CIFR) with a hold rating, noting that the miner’s potential HPC hosting deal at its 300 MW Barber Lake site is already “priced in.”

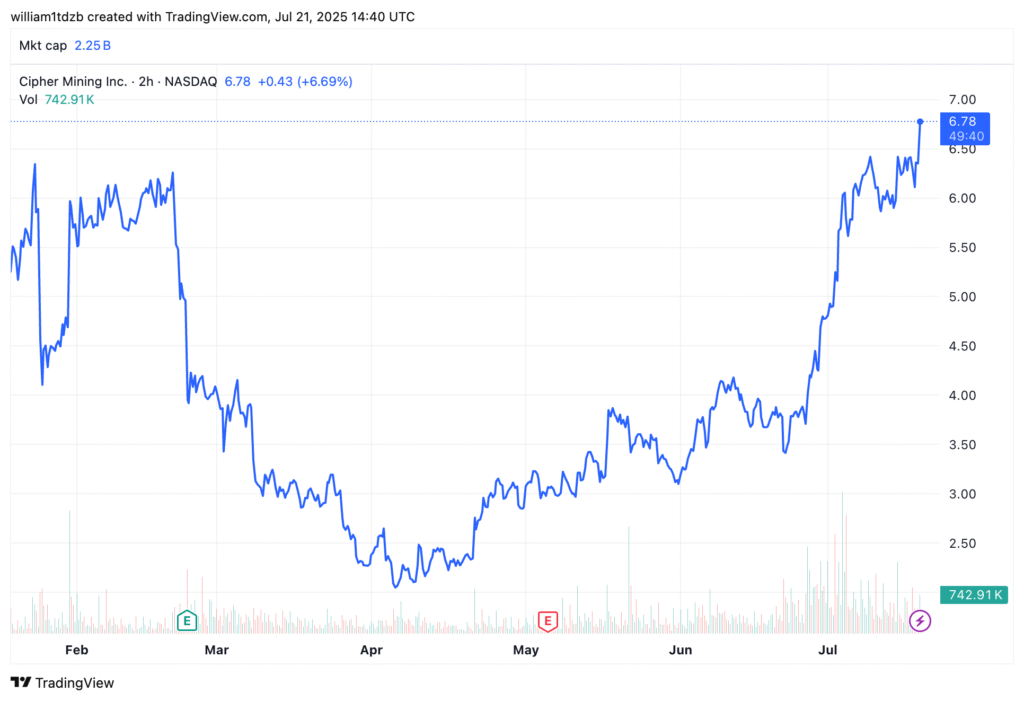

Shares of Cipher Mining have climbed over 65% since late June and nearly 200% from their April lows, which Jones argues is now fairly priced. Jones does not assign price targets to hold-rated stocks.

According to Jones, CIFR has traded at a EV/EBITDA multiple of 19.6x–26.4x for 2025 at hashprice levels ranging from $45/PH/day to $55/PH/day, well above the hybrid AI-mining peer average of 13.3x–21.8x.

Jones sees a potential build-to-suit lease joint venture (JV) with an HPC hyperscaler at Cipher’s Lake Barber facility, where Cipher would contribute $150 million for a 25% initial stake, rising to 40% on milestones. Jones DCF analysis values potential JV equity at $2.23 billion after debt, implying $558–$893 million of equity value for Cipher (or $1.50–$2.41 per share).

Beyond Barber Lake, Jones believes Cipher’s 1.67 GW Texas pipeline—including its 100 MW Stingray site and 70 MW Reveille site—faces hurdles. They are smaller scale, non-tier 1 locations, Jones argues, with undisclosed fiber and water spec that face competition from Galaxy, IREN, Riot, and Crusoe. Jones’ says it would turn “incrementally positive” if these execution risks diminish.

With stock momentum likely to persist on a deal announcement or rising hashprices, Jones says, Cipher’s risk and reward appears balanced, meriting a hold.

At time of publication, CIFR is up 7% from yesterday’s close.