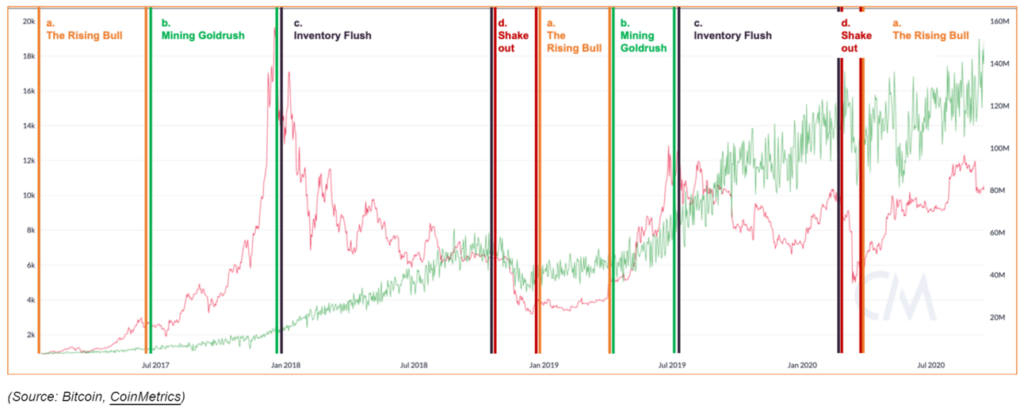

The mining cycle continues. Mining analysts have identified a cyclical boom-bust pattern to Bitcoin mining ever since Bitcoin entered the “modern” post-ASIC era (~2014). Around the 2020 halving, a cycle model was codified by the Coinmetrics and Alkimiya teams and consists of 4 seasons:

- The Rising Bull

- Mining Goldrush

- Inventory Flush

- Shake Out ← You are here

Many analysts, myself included, were surprised to see hashrate continue to skyrocket from the FTX bottom in late 2022 to the April 2024 halving. Hashrate nearly tripled from 240 EH/s to 640 EH/s in a relentless climb, seemingly unaffected by price & sentiment collapse. In hindsight it is clear that this was the “Inventory Flush” period.

Inventory flush due to overproduction happens in many markets that suffer from high reaction delay. Miners were able to tap into previously inaccessible sources of capital, namely public markets, to stave off bankruptcy meanwhile ASIC manufacturers like Bitmain continued to ship units. This resulted in a significant glut of machines available to the market and a significantly lower rig price environment that still shows no sign of recovering.

We are finally seeing hashrate decline. After the April 2024 halving mining profitability collapsed in all 3 significant revenue drivers:

- Block subsidy down 50%

- Bitcoin Price down 20%

- Fees per block down 50%

All these combined mean miners are generating about 50% less revenue today than they were over the past year. This is resulting in the first 2 consecutive negative difficulty adjustments since June 2022 (!) and about a 15% decline in hashrate from the April 2024 peak.

We’re officially in the “Shake Out” phase.