The April 2024 halving marked more than just a reduction in block rewards. Bitcoin’s price soared past $100,000, yet miners faced a challenging trifecta: a 50% revenue cut, relentless growth in network difficulty, and historically low transaction fee rewards.

With rising competition and revenue uncertainty, miners faced razor thin margins and they are still skating on the edge more than a year out from the event, while some are adopting more sophisticated hedging strategies to weather the volatility.

Here’s what has changed since the 2024 halving.

The halving and its fallout

The bitcoin halving immediately cut bitcoin mining revenue in two. Despite this, Bitcoin’s total network hashrate has continued to grow at a time when transaction fees are at multi-year lows, which has put further pressure on hashprice.

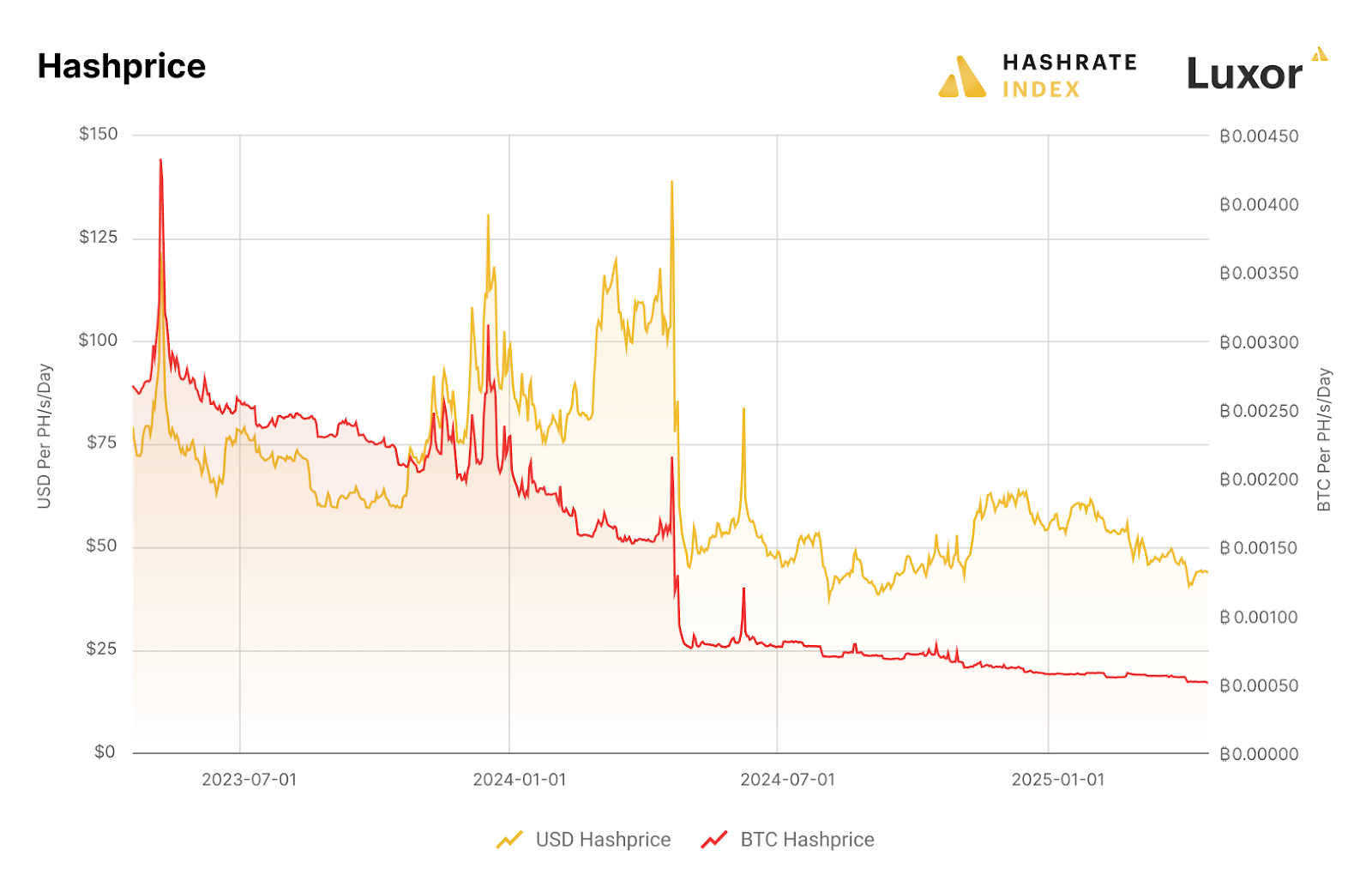

Hashprice is a mining metric that quantifies how much a miner can expect to earn from a specific quantity of hashrate. This metric captures the combined effects of changes to bitcoin price, network difficulty, and transaction fees (and in the case of the halving, the block subsidy) into a single revenue measurement, denominated in either USD or BTC per PH/s/Day.

Hashprice is positively correlated with changes to Bitcoin’s price and transaction fee volume but negatively correlated with changes to network difficulty.

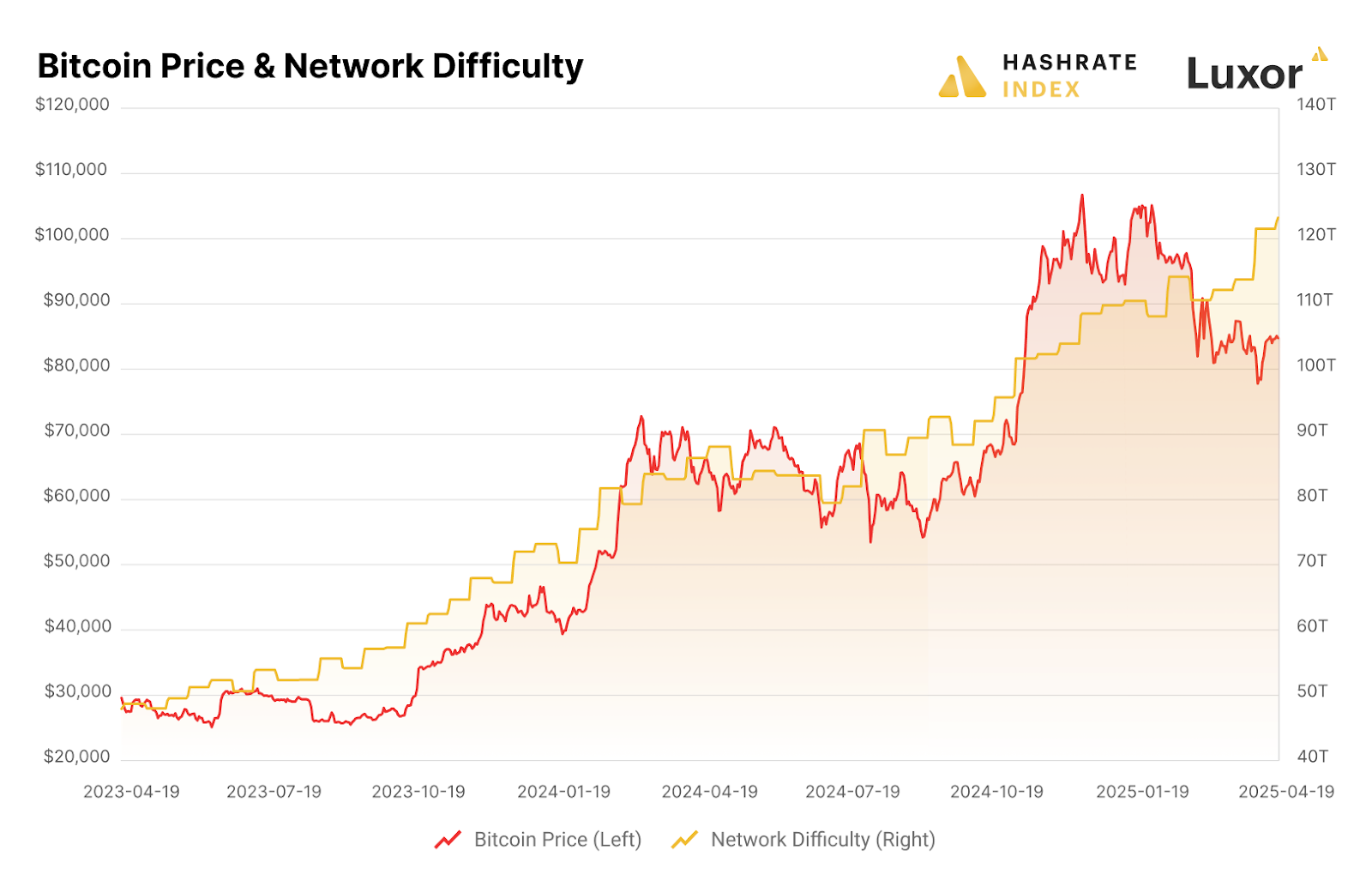

Between April 2023 and April 2025, Bitcoin’s daily price more than tripled, averaging ∼ $57,500. However, this bullish momentum was met with an equally aggressive rise in network difficulty. These forces grappled with each other, wrestling hashprice downward and adding to the pressure inflicted by the halving.

Bitcoin’s difficulty was 86.39T at the time of the halving, with roughly 618 EH/s online at the time of the event (according to the 7-day average). A year later, difficulty had increased 43% over the period to an all-time high of 123.23T at 882 EH/s.

Source: Hashrate Index

One of the more surprising post-halving developments was a sharp decline in transaction fee volume. Between April 2023 and April 2025, average transaction fees collected (per block, per day) fell 70%, from 0.550 BTC to 0.165 BTC.

Pre-halving, transaction fees as a share of total block rewards averaged 7.12%; post-halving, that fell to just 4.02%. Despite isolated fee spikes from runes and ordinals activity, the reduced fee market environment diminished miner revenues.

The increase in difficulty and low fees overwhelmed hashprice despite the positive bitcoin price action. As a result, hashprice has had a difficult time recovering since the halving. USD hashprice averaged $66.35/PH/day between April 2023 and April 2025, and it is roughly ∼$45/PH/day at the time of writing. Meanwhile, BTC hashprice averaged 0.001462 BTC/PH/day, and is currently ∼0.000517 BTC/PH/day.

Overall, USD and BTC hashprice have fallen 57% and 89%, respectively, since April 2024. This steep decline has compressed revenue for miners, especially those relying on FPPS (full-pay-per-share) payout models.

BTC-denominated hashprice underperforms forward market expectations, while USD outperforms

In the year since the April 2024 halving, one significant development in bitcoin mining was the growth of the hashrate forward market. This market enables miners to hedge and reduce exposure to hashprice. Lenders, investment funds, and proprietary traders tend to participate on the buy side; whereas public and private miners are active on the sell side, either to hedge or receive financing for ASICs fleet expansion.

Historically, mining revenues were highly sensitive to hashprice, which made it difficult for operators to forecast cash flows or secure financing. Hashrate forward markets enable miners to sell future hashrate production at a fixed hashprice, locking in revenue months in advance. This financial instrument functions similarly to commodity futures in the energy sector, where electricity producers pre-sell power contracts to stabilize income.

As with traditional commodities markets, hashrate forward contracts allow bitcoin miners and traders to buy or sell the future production of a bitcoin mining operation at a fixed, pre-agreed cost.

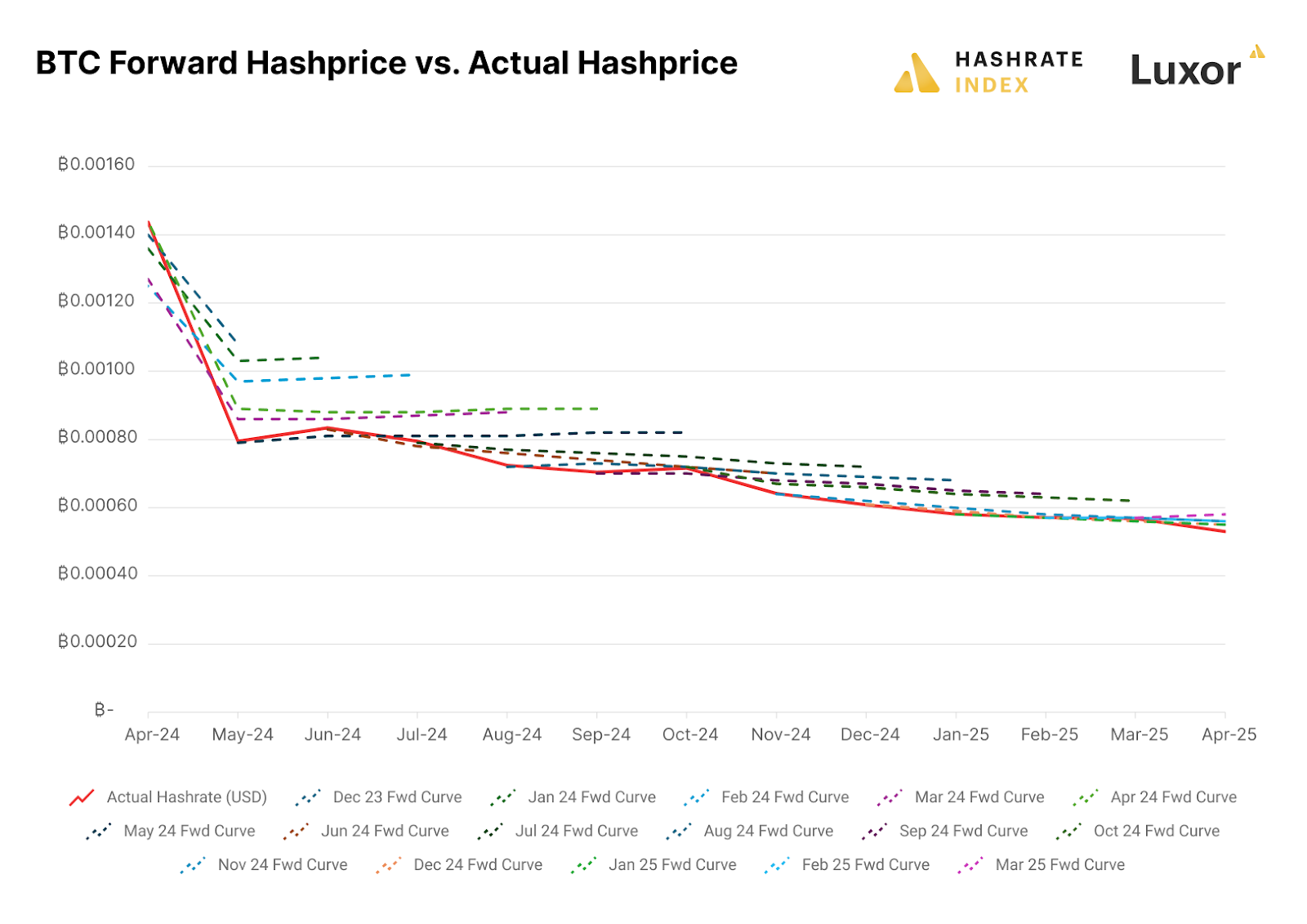

Performance in hashrate forward markets convergence at the nexus of expectation and reality. Following the April 2024 halving, mining market participants were met with surprise. Network difficulty consistently outpaced expectations while transaction fees fell short. These headwinds significantly compressed mining margins.

Consequently, actual BTC-denominated hashprice was consistently lower than forward market expectations, as shown in the chart below.

With significant bitcoin price volatility since the halving, the story was a little more complicated for USD-denominated hashrate forward markets. In particular, the post-election surge in bitcoin price caused USD-denominated hashprice to exceed forward market expectations in Q4-2024 and at the start of 2025.

These misalignments between expectation and reality directly influenced miner outcomes. Actual BTC hashprice declined more sharply than expected, and this persistent basis between forward and spot BTC hashprice revealed the optimal strategy: locking in fixed BTC payouts. This strategy allowed miners to guarantee a hashprice before difficulty continued its sustained climb, effectively mitigating the subsequent spot hashprice decline.

What do hashrate forward markets tell us about the future of hashprice?

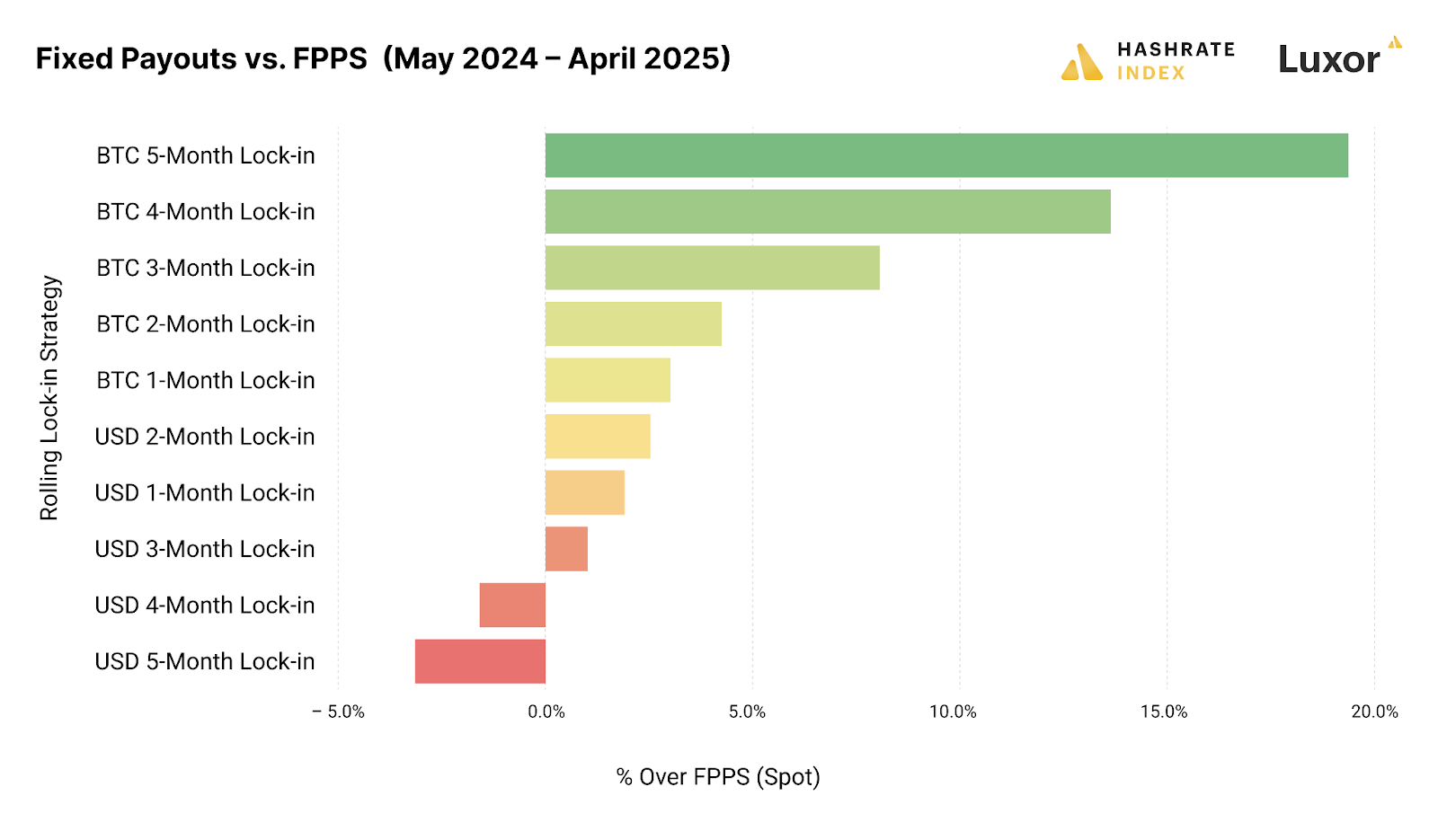

Mining pools with fixed payouts enable their miners to use the hashrate forward market by locking in a hashprice. Continuously entering into a series of fixed payout contracts effectively locks in revenue over an extended time period for the miner. Post-halving, these “rolling lock-in” strategies delivered measurable results.

The chart* below summarizes how different hashrate hedging strategies (segmented by denomination and time horizon) performed between May 2024 – April 2025, relative to FPPS (spot) mining:

*Note: This information is for demonstration purposes only and excludes fees and bid/ask spreads associated with entering into hashrate forward contracts.

Between May 2024 and April 2025, fixed payout contracts denominated in BTC consistently outperformed FPPS, with longer lock-in durations delivering the strongest results. A rolling five-month BTC lock-in strategy delivered nearly 20% more than FPPS, while four and three-month terms also significantly exceeded spot rates.

USD-denominated contracts showed a different pattern. Shorter lock-ins offered modest outperformance, but performance declined with longer durations, turning negative for four and five-month terms.

The takeaway: miners who locked in BTC payouts over multi-month periods captured the greatest upside during this volatile post-halving period.

A caveat: Although selling forward proved to be favorable in this timeframe, it is critical to recognize that hedging is typically a cost of business rather than a revenue generation method. Hedgers willingly pay a price to buy certainty and obtain more predictable cash flows, which tends to increase valuation, reduce cost of capital, and ultimately attract investments.

But that’s all in the past. What of the future?

Looking forward, Luxor’s hashrate forward market is pricing in an average hashprice of $50.57 or 0.00053 BTC per PH/s/Day over the next six months.

Disclaimer

This content is for informational purposes only, you should not construe any such information or other material as legal, investment, financial, or other advice. Nothing contained in our content constitutes a solicitation, recommendation, endorsement, or offer by Luxor or any of Luxor’s employees to buy or sell any derivatives or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the derivatives laws of such jurisdiction.

There are risks associated with trading derivatives. Trading in derivatives involves risk of loss, loss of principal is possible.